Vodafone and TPG merger, Australia

28.08.2020Background

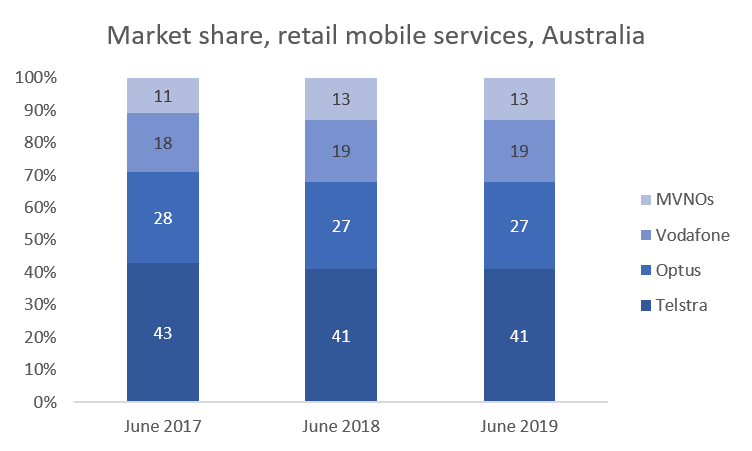

Source: ACCC 2019: 31.

TPG Telecom Limited (TPG) has operated as a retail service provider in Australia for many years, as both an infrastructure owner and operator – such as local access and submarine fibre cable networks – and as a reseller of services supported by other networks. TPG has acquired its own radiofrequency spectrum suited for the provision of mobile services.

Vodafone Hutchison Australia Pty Limited (Vodafone) is a mobile network operator. It operates a third mobile network in Australia and has for several years had a market share of just under 20 per cent in the mobile services market, after Telstra and Optus. Vodafone has struggled to improve its market position.

In September 2015, TPG and Vodafone jointly announced that they had signed two agreements which would enable them to enter into what has been referred to as an “operational merger.” Under the first agreement, the Dark Fibre Agreement, TPG would provide dark fibre and network services to more than 3 000 Vodafone sites over a 15-year term and, to enable this, TPG proposed to extend its fibre infrastructure by constructing about 4 000 kilometres of new fibre to Vodafone cell sites across Australia. Under the second agreement, the MVNO Agreement, the two companies intended to create what they described as “one of the industry’s largest-ever Mobile Virtual Network Operator (MVNO) arrangements,” under which TPG would migrate its mobile wholesale customer base to the Vodafone network. TPG customers would have access to Vodafone’s 4G services, a service not always available to MVNOs hosted on other mobile networks.

A further scheme was entered into between TPG and Vodafone in August 2018, which proposed the establishment of a merged entity. It was a condition precedent of the scheme that Vodafone should obtain a merger clearance from the Australian Competition and Consumer Commission (ACCC).

Australian competition law

On May 8, 2019, the ACCC announced that it declined to give informal merger clearance on the basis that the merger would be likely to have the effect of substantially lessening competition in the supply of retail mobile services in Australia, in contravention of Section 50 of the Competition and Consumer Act 2010 (CCA).

Vodafone appealed the decision and sought declaratory relief from the Federal Court. The case differed from the run of the mill merger cases in that the ACCC had refused to give an informal clearance, but it had not actually disallowed a merger. The effect, however, was the same.

The evidence

The ACCC, in applying the substantial lessening of competition (SLC) test, had to compare forecasts or scenarios to determine the competitiveness of the mobile services market if the merger proceeded and if it did not. The SLC test required the ACCC to show, on the balance of probabilities, that the scenarios it conceived were the most likely, and that one involved a level of competition substantially below the other, sufficient either to justify clearing the merger or to justify preventing the merger.

The ACCC contended that, without the merger, TPG would build its own network and compete fiercely on that basis against all three existing mobile network operators (MNOs). This would cause the existing MNOs to retaliate and, in the process, to increase the overall competitiveness of the market. With the merger, the ACCC contended that TPG would not build its own network and there would likely be no further market entry, TPG being the only potential new facilities-based entrant. Thus, the ACCC concluded that the overall level of competition would be lessened if the merger proceeded.

In the hearings, TPG gave evidence that its role in the market as an MVNO had been consolidated over a number of years but stated that it had no plan or intention of building its own network in the absence of a merger with Vodafone. Therefore, according to Vodafone, the comparison used by the ACCC was incorrect. The comparison should have been between a scenario (without the merger) in which the current level of network competition continued unchanged, and a scenario (with the merger) in which competition would be enhanced as a result of a more competitive third mobile network hosting a strengthened MVNO.

Federal Court decision

The Federal Court upheld the application by Vodafone and overruled the ACCC’s decision (FCA 2020). The court determined that it was able to rely in the evidence of the TPG witnesses, in particular that there was no real likelihood of TPG establishing its own network in the absence of the merger. Once the court reached this assessment, one that it would likely reach in any similar case if the credibility of the witnesses was not impugned, then the comparison of the future levels of market competitiveness maintained by the ACCC became untenable. The merger did not remove, or alter in any way, the potential entry of a fourth mobile network operator, because TPG was never going to be that entrant in any relevant timescale. On the other hand, the merger would likely strengthen the position in the wholesale market of the existing third network operator, Vodafone, and strengthen the position in the retail market of the existing MVNO, TPG.

The court concluded (FCA 2020: 898):

- MergeCo[1] will have the financial capacity required to deploy 5G more quickly, providing the capacity uplift required to provide a competitive service. The increase in the capacity of MergeCo’s network will reduce the need to build additional sites or conduct ‘tactical’ 4G upgrades to relieve immediate congestion issues, a substantial proportion of which is inefficient as it would need to be also replaced in the near future. That will release additional capex which can be directed towards accelerating MergeCo’s 5G roll-out. MergeCo’s access to 60 MHz of 3.6 GHz spectrum will also enable it to provide a higher quality 5G service with faster speeds for many more years than Vodafone or TPG could offer alone.

The judge then provided a detailed analysis of the evidence and concluded that, in many market segments and service offerings, the merged entity would have much improved ability to compete with Telstra and Optus than Vodafone and TPG operating as now (FCA 2020: 898).

The ACCC subsequently announced that it did not intend to appeal.

Wider significance of the case

This case in many ways is typical of the approach that regulators and courts have taken to assessing whether mergers and acquisitions are in the public interest and to the application of the SLC test. The case illustrates the difficulties in developing compelling forecasts or scenarios of the impact of competitiveness in a market with and without the proposed merger. Detailed case-specific assessment is required, of the kind that the judge undertook and recorded in his decision.

The case also indicates the challenges inherent in applying the SLC test when one or both scenarios is heavily dependent on the plans or assumed plans of the merging firms. Provided the integrity of the firms’ witnesses cannot be reasonably impugned, it is difficult, if not impossible, to show that the firms would have invested in significant separate infrastructure in the absence of a merger. This aspect of merger regulation will be an increasingly important challenge in the digital platform era as global scale becomes a standard measure.

The Vodafone case concerned the third of three operators in a market. However, in other circumstances it might have concerned a merger by a (national) market leader trying to improve scale and bargaining leverage to negotiate more effectively with global platform behemoths. National competition agencies and national courts appear, in most cases, not to have the tools to address the issues involved in such a case. With global online platforms increasingly influencing the dynamics of this and other markets defined under legacy rules, it will be harder for any national regulator to have enough robust data to credibly undertake the thought experiment associated with the substantial lessening of competition test. As the ACCC discovered, even now it can be almost impossible.

Endnotes

- The name given to the operating entity to be established ↑

References

ACCC (Australian Competition and Consumer Commission). 2019. ACCC Communications Market Report, 2018-19. Melbourne: ACCC. https://www.accc.gov.au/system/files/Communications%20Market%20Report%202018-19%20-%20December%202019_D07.pdf.

FCA (Federal Court of Australia). 2020. Vodafone Hutchison Australia Pty Limited v Australian Competition and Consumer Commission. [2020] FCA 117. https://www.austlii.edu.au/cgi-bin/viewdoc/au/cases/cth/FCA/2020/117.html.

Last updated on: 19.01.2022