Evolving business models in the ICT sector

31.08.2020The increasing digitalization of the way we work and live also impacts the way we communicate. Instead of making traditional voice calls and sending 160 character SMS messages, people can communicate more conveniently, with full video and in groups using Internet applications. Services that were previously provided by mobile network operators (MNOs) now face competition from the public Internet. Voice calls and SMS have to compete with over-the-top (OTT) applications, such as Skype, WhatsApp, and Facebook Messenger. Cryptocurrencies based on blockchain technology may compete with mobile money. The business models of domestic connectivity providers need to adjust to these new services, as do regulators, who have to reconsider their scope of responsibilities.

MNOs are mobile Internet service providers (ISPs) and data are the primary source of revenues. The mobile business model will follow that of fixed-line operators, which started out as voice service providers but now make their money mostly from data connectivity, either retail or wholesale. Over the past two decades, the majority of MNO investment has gone into data networks. The transition from a voice and SMS to datacentric-business model is inevitable (see table below).

The Evolving Digital Business Model is Inevitable

| Analogue mobile | Digital mobile | |

| Business model | Service | Connectivity |

| Metric | Minutes and SMS | Bandwidth or throughput |

| Cost sensitivity | Distance, duration, and location matter | Time, distance, and location insensitive |

| Billing | Access and usage billing: detailed billing systems for voice and SMS that can distinguish between off-net/on-net, peak/off-peak | Simple access billing |

| Traffic monitoring | Detailed traffic monitoring as part of the billing system | Usage monitoring limited to data use |

| Postpaid subscribers | Detailed vetting to reduce risk or revenue loss and expenses that arise from call termination and subsidized handsets |

|

| Network infrastructure | GSM 1G and 2G | 2.5G, 3G, 4G, 5G |

Source: Esselaar and Stork 2019.

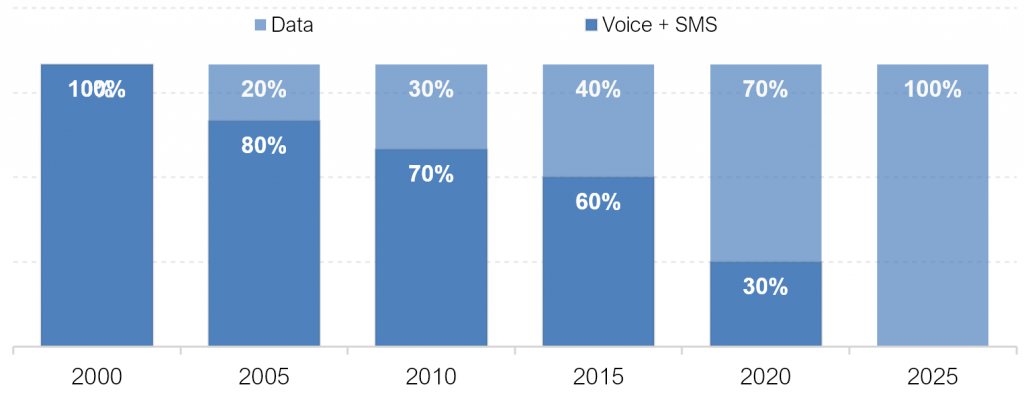

MNOs will eventually entirely become mobile Internet access providers, distinguishing their products by speed and quality of service, and competing with other forms of access, such as public Wi-Fi and connectivity in places of work, study, and the home. MNOs will no longer charge for voice and SMS, only for bandwidth and/or data consumption. The mobile ISP business model can also be described as a datacentric or a digital business model. The figure below illustrates this transition.

Illustrative trends towards digital mobile business models

Source: Esselaar and Stork 2019.

Apart from competitive pressure, this trend also depends on smartphone penetration and 3G+ network coverage. The migration to a digital mobile business model will take longer for countries that have little 3G, 4G, and public/private Wi-Fi coverage, and low smart phone penetration. Insufficient 3G+ network coverage is one of the main reasons why some mobile operators struggle to generate enough data revenues to compensate for declining voice and SMS revenues.

The digital business model is all about knowing the customer. The actual battle is not that of cannibalization of one product for another, i.e. replacing voice and SMS with data revenues, but one of maintaining information on subscriber leadership. For years, MNOs were in the lead, knowing where their customers were in space and time, whom they communicated with and when. While this information is still available to MNOs, social media and online shopping provide a more potent and detailed information source. The information that Amazon and Facebook have about a customer is likely to be more economically valuable than the information that an MNO has about the same customer. To enter this market is a business decision, not a regulatory decision.

EBITDA (earnings before interest, taxes, depreciation, and amortization) margins along the Internet value chain show that end-user access is still a profitable business. More important than the size of each segment in terms of revenues is the profitability of major players in each of the value chain segments. The table below displays the EBITDA margin for selected players for each of the value chain segments. On average, EBITDA margins for connectivity are higher than the other segments of the value chain. It would be difficult to argue that MNOs are facing more adverse conditions than other segments. The variance of EBITDA margins between segments also shows that each segment has its own value proposition, investment criteria, and returns. Netflix, for example, is much more profitable than Disney.

EBITDA Margin Along the Value Chain Based on Audited Financial Statements (%)

| Segment | Company | 2016 | 2017 | 2018 |

| Content rights | Netflix | 60 | 61 | 59 |

| Warner Media | — | — | 18 | |

| Disney | 30 | 30 | 29 | |

| Fox Corporation | — | — | 22 | |

| Online services | Amazon | 9 | 9 | 12 |

| Alphabet | 33 | 30 | 26 | |

| 53 | 57 | 52 | ||

| Enabling technologies | Cisco | 30 | 30 | 31 |

| Akamai | 41 | 37 | 40 | |

| Connectivity | Airtel Group | 35 | 38 | 37 |

| Etisalat | 50 | 50 | 49 | |

| Maroc Telecom Group | 48 | 49 | 50 | |

| MTN Group | 35 | 33 | 35 | |

| Ooredoo | 41 | 42 | 41 | |

| Sonatel | 49 | 47 | 45 | |

| Safaricom | 42 | 48 | 48 | |

| Vodacom Group | 38 | 38 | 38 | |

| Average Connectivity | 42 | 43 | 43 | |

| User interface | Apple | 33 | 31 | 31 |

| Samsung | 24 | 31 | 35 |

Source: Esselaar and Stork 2019.

As MNOs transition into a fully datacentric model, they can expect their profit margins to decline to the levels of other segments of the value chain. The transition to a datacentric model also means less need for ICT sector-specific regulation. With the exception of the radio spectrum, telecommunication regulation will become less sector specific over time.

References

Esselaar, S. and C. Stork. 2019. “Evolving Business Models are Driven by OTT Applications.” Paper presented at the ITU Study Group on OTT, Geneva, September 2019. https://researchictsolutions.com/home/wp-content/uploads/2019/11/RIS-evolving-business-models.pdf.

Last updated on: 19.01.2022